ZOPA v Savings accounts

Estimated returns over time on ZOPA & other savings accounts

A bit about ZOPA & me to start;ZOPA was established 7 years ago in March 2005, ZOPA's explanation of how it works is: "People put money in. Borrowers borrow money. Everyone is happy." This may sound very simplistic but it's fairly accurate.

I have been saving with ZOPA, in a small way since 2007. I generally blog about saving (investing) smaller amounts of money in simple & safe or very safe ways, for the medium & long term.

ZOPA explains how it all works on their web site, in a much better way than I can do in this post, so if you want more details about them click here. If you want more background on the history and detail of Social Lending or Person-to-Person (P2) lending then Wikipedia also has a great article which includes other organisations. As of July 2012 there are around 35 competitor peer-to-peer lenders set-up around the world.

Why 'risk' money in ZOPA or anything else for that matter?

This is a bit about personal choice & of course the amount of money you have to save. I would suggest that your money is at some risk wherever it is. If it's in a high street bank or building society account then the risk is very low but there still is a risk. A low risk almost always means very little reward, so you will only get a low rate of interest on these accounts. My personal attitude to saving, or 'investment' to use a different term, is that I'm prepared to accept a small amount of risk to get a reasonable return over time.Interest rates are really important over longer periods of time because of the effect of compound interest. You could of course keep your cash under your mattress (apart that it might get stolen) but then you are actually losing money over time because;

"Except for rare periods of significant deflation where the opposite may be true, a pound (£) in cash is worth less today than it was yesterday, and worth more today than it will be worth tomorrow." (Source: Wikipedia; Rate of Return)So, what I'm looking for is a reasonable rate of return (interest rate) for the lowest possible risk as I don't really want to lose my money :) Therefore I would prefer to protect most of my capital (like it is in a savings account) rather than for example invest in the stock market when my capital isn't protected.

So that's enough background time to look at some of the data that I've researched on long term Interest rates from UK savings accounts and what ZOPA has to offer.

Interest Rates

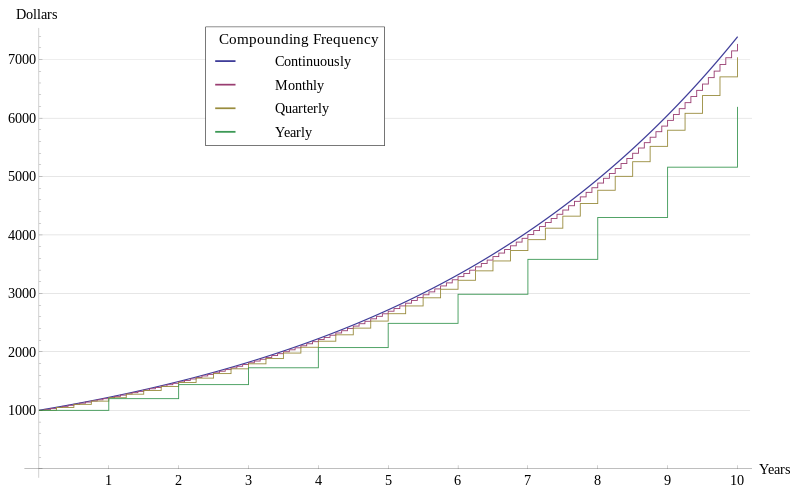

In short; even when the unusually high interest rates that were on offer during the late 80's & early 90's are included ZOPA's average return is still slightly higher than savings accounts. This is especially true now (July 2012) when general interest rates are at historical lows & looking to stay that way for a long time yet.Looking at rates from March 2003, when ZOPA started, ZOPA's return is; 2.7 % higher than the best on offer from UK savings accounts. If you just look at the last three years, since the start of the economic troubles, then it's a slightly better return from ZOPA which is; 2.9% higher than savings accounts. You may think that 2.9% doesn't sound like much, maybe not worth the hassle? But according to Einstein; “The most powerful force in the universe is compound interest.” So over a few years 'compound interest' makes a difference, in fact it can make a lot of difference. For example if you had £1000 invested over 10 or more years:

| Years | Investment | Highest | Lowest | ZOPA 3Yr | Avg 3Yr |

| 10 | £1,000.00 | £3,782.70 | £1,311.65 | £1,740.80 | £1,313.78 |

The last two cells above (ZOPA 3yr & Avg 3yr) show the difference that even a small percentage of 2.93% can make over a period of 10 years, in this case you would be £427.02 richer with your money invested in ZOPA.

Looking at the same investment amount of £1000 but over much longer terms of say 20 or even 50 years, which are the typical saving periods for a child's University fees or for retirement:

| Years | Investment | Highest | Lowest | ZOPA 3Yr | Avg 3Yr |

| 20 | £1,000.00 | £14,308.81 | £1,720.43 | £3,030.39 | £1,726.02 |

| 50 | £1,000.00 | £774,477.56 | £3,882.32 | £15,986.35 | £3,913.93 |

As you can see the effects of compound interest real kick in here with some very, very large differences appearing over time. Of course it would be almost impossible to sustain the highest interest rates over a period of 50 years but if you could do it, you would be very rich indeed. What I think this shows and I hope you agree, is that a small percentage increase can make a big difference over time so it's worth shopping around for the best interest rate on offer for your money. (I'll do another post looking at a more typical situation where you save small amounts regularly over time, rather than starting with a lump sum.)

One thing to think about here is that the reverse is true of your mortgage or other longer term borrowing. The longer you have it and the higher the interest rate (even a little higher) can make a big difference, so paying your mortgage off early can literally save you thousands of pounds. Especially if your mortgage interest rate is higher than your savings interest then it may make sense to use your savings to pay off your mortgage early .

There is some small print I ant to make you aware of here with ZOPA: If you sign up to ZOPA through the links on this and other pages in this blog then they might pay me an introduction fee of £50.00 (Woo! Every penny helps especially if they are compounded up over many, many years :) This won't cost you anything at all and it helps me keep the blog going. The T&C's are available here but basically: "each existing Zopa member who introduces another person to Zopa will receive £50 when that person either lends at least £2000, or borrows any amount of money, at Zopa during the Offer Period, provided that this person has signed up via the existing member's referral page supplied by us to you."

.png)